InMode Ltd. - The Cannibal in the Waiting Room

Long-term compounder or DOA?

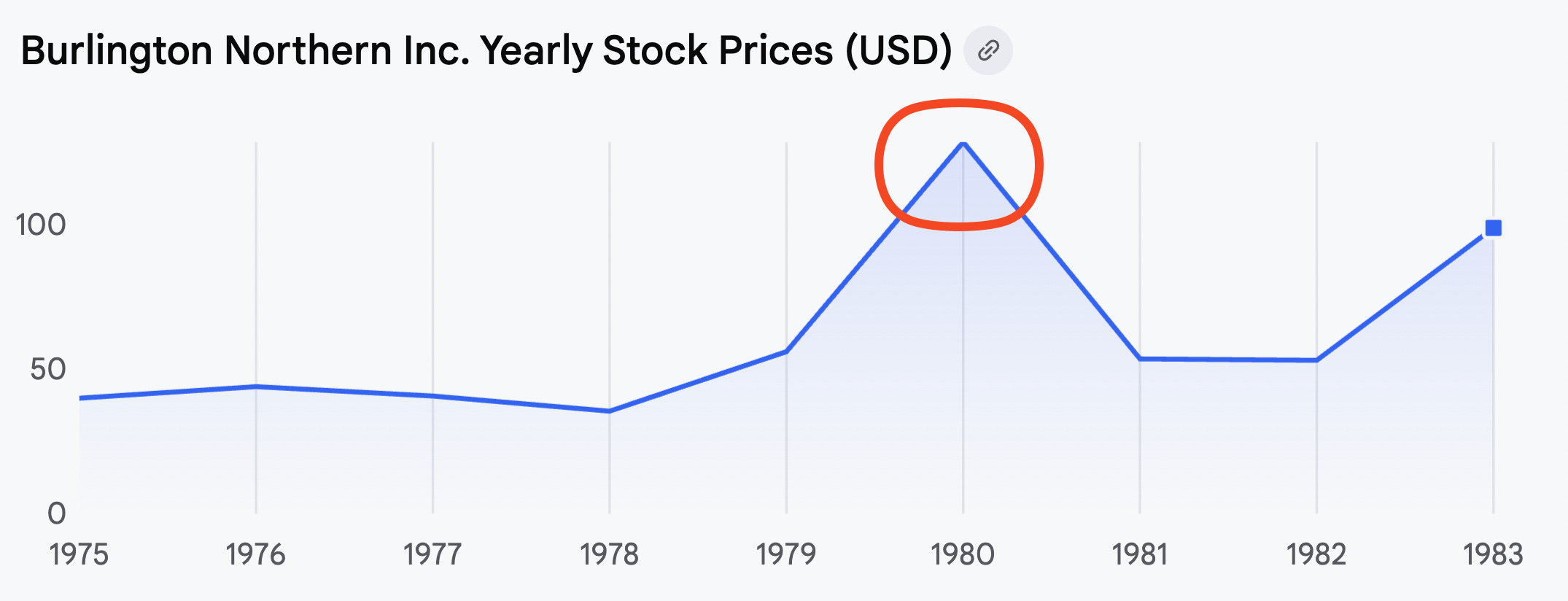

In 1980, Burlington Northern Railroad did something that looked, to most observers, like slow-motion suicide.

Instead of laying new track, buying competitors, or chasing empire-building growth, they started ripping up the floorboards. Routes were abandoned. Land was sold. The network shrank by roughly a third.

Wall Street was horrified. Railroads were supposed to be about scale… More cities, more reach, more iron. A shrinking railroad sounded like a dying railroad.

But something unintuitive happened to Burlington Northern’s shareholders: They got rich.

By shedding unprofitable routes and concentrating investment on the lines that actually printed money, the company generated more cash with less track. And when a business throws off cash while the market hates it, a second powerful lever appears… Management can buy back shares for pennies on the dollar.

Sure, the enterprise gets smaller, but your slice of the pie gets exponentially larger.

This is the gap between how we talk about businesses and how we experience returns. Human psychology equates health with more: More revenue, more headcount, more footprint. When something contracts, ancestral survival mechanisms kick in and we instantly recoil.

But ownership returns are not measured in empire size. They’re measured in free cash flow per share.

That brings us to InMode (INMD).

InMode dominates the market for minimally invasive aesthetic hardware. Specifically, Radio-Frequency (RF) and laser technology used for body contouring and skin tightening. Over the last decade, it has built its own “track” by selling around 29,000 systems in clinics worldwide.

But there’s a catch. A laser is not a railroad.

Burlington Northern had a monopoly on physical geography. Rail tracks don’t go obsolete; they last 50 years. InMode is selling technology in a viciously competitive market. Tech obsolescence is the enemy. A laser is not a permanent asset; it is a melting ice cube.

As a result, InMode is playing a much faster, more dangerous version of the railroad game. The biggest question on investors’ minds is: “Can they retire share count faster than technology ages?”

The bet isn’t that InMode is a “forever asset.” It’s that the share count shrinks faster than the technology becomes obsolete.

A Funeral Price on a Company With a Pulse

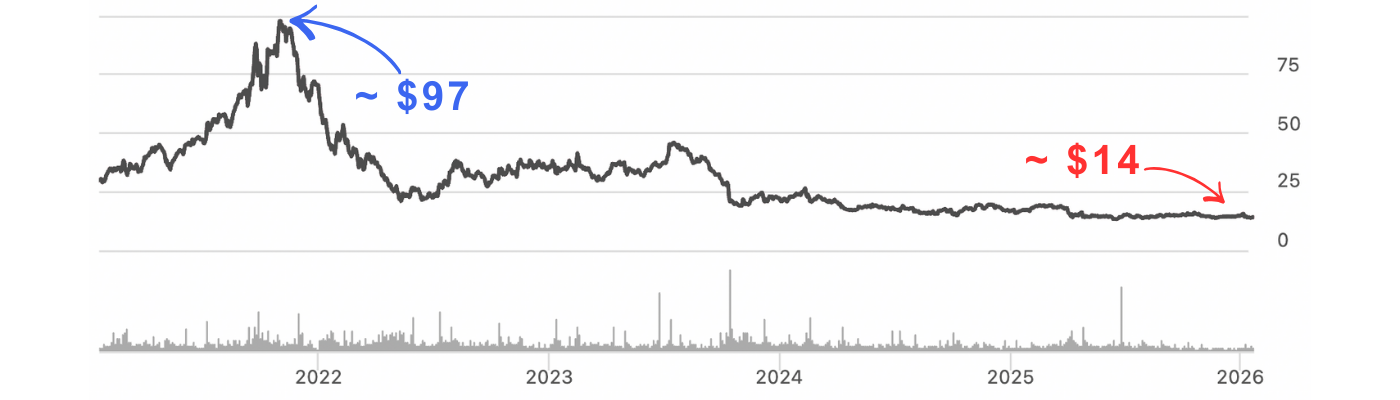

InMode is priced like a company with a broken future. The stock is down ~85% from its highs, and revenue fell off a cliff in 2024. Sentiment is so toxic that investors talk about the business in the past tense.

But the market’s narrative is clean, logical, and emotionally satisfying: GLP-1 drugs changed the world.

The logic goes like this…

If people can lose weight with Ozempic, demand for aesthetic procedures must shrink. If procedures shrink, clinics stop buying equipment. If clinics stop buying equipment, the business evaporates.

But that narrative ignores the physics of rapid weight loss.

GLP-1s are fantastic at melting fat but terrible at shrinking skin. Rapid weight loss leaves patients with sagging skin. You cannot exercise away loose skin. You have two options: Expensive surgery or RF skin-tightening (InMode).

GLP-1s don’t necessarily destroy InMode’s market; they potentially create a massive new cohort of patients who need skin tightening after the weight loss.

The “Elephants in the Room”

If the GLP-1 narrative were the only issue, the stock likely wouldn’t be trading at ~4x ex-cash earnings. The market is pricing in two existential threats that don’t show up on the P&L:

The “Israel Discount”: InMode is HQ’d in Yokneam. In the current geopolitical reality, many institutional mandates are structurally forbidden from owning the stock. The market is treating the $500M+ cash pile not as an asset, but as “trapped” or “at risk” capital.

The Litigation Shadow: The aesthetics industry is a magnet for lawsuits. Short reports and patient claims regarding burns or scarring create a “tail risk” shadow that scares away conservative money.

Here’s the contrarian take: The market isn’t ignoring these risks; it’s pricing them in. At this valuation, you’re not paying for a pristine outcome. You’re paying for a distress scenario. The upside is that reality is less severe than what’s implied.

The real question isn’t whether InMode returns to hyper-growth…

It’s whether InMode keeps the lights on long enough to buy back half the company.

The Business Model: Museum vs. Toll Road

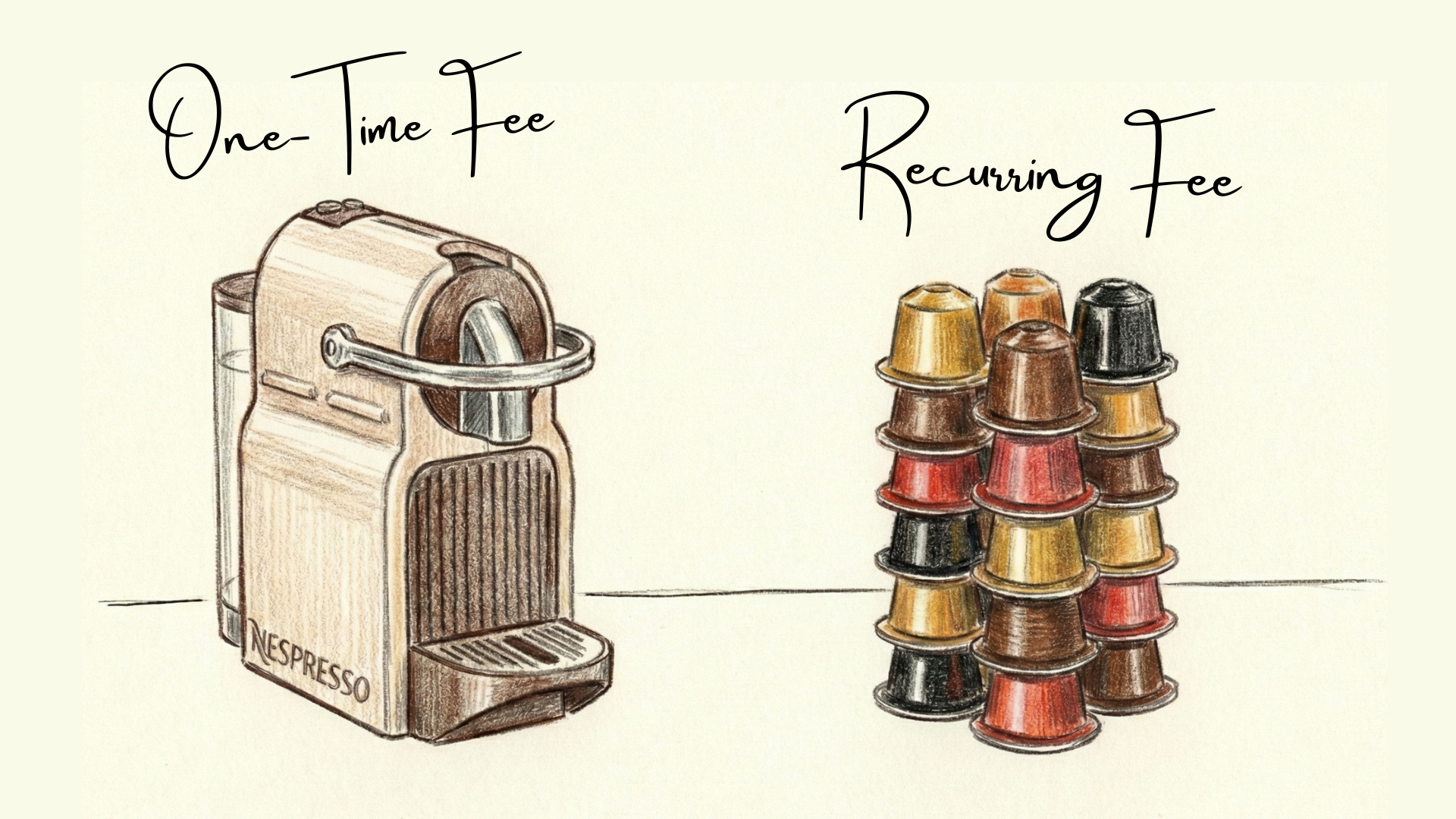

InMode sells high-ticket radio-frequency platforms to clinics. That revenue is cyclical, financing-sensitive, and currently weak.

It’s not the one-time sale that matters… It’s the recurring fee (the real business).

Many procedures performed on InMode systems require proprietary single-use consumables, such as tips, handpieces, and disposables. These are not generic; they are DRM-locked to the machine. Every time a clinic turns the machine on, InMode gets paid.

The thesis doesn’t need equipment sales to grow… It just needs those 29,000 units sitting in offices to be put to use.

This is the dividing line…

A large installed base that sits idle is left for dead, while a large installed base that stays busy is a toll road.

For this “Cannibal” thesis to work, three things must hold:

Utilization: Consumables revenue must stay healthy relative to the installed base. If consumables weaken, the doctors have stopped using the machines, and the recurring revenue dies.

Margins Stay High: The buyback engine runs only when the business converts revenue into cash. If margins crash, the fuel for buybacks disappears.

Management Doesn’t Get Bored: The entire point is that depressed sentiment makes the equity cheap. If management uses cash to buy a competitor or to pivot rather than buy back its own cheap stock, the thesis breaks.

INMD Investor Pack: The Mechanics of the Trade

The Thesis in One Paragraph: INMD is being valued as if it were a dying company. The real bet is that the company can compound per-share value through:

(1) Durable cash generation from an active installed base, and

(2) Aggressive equity retirement at distressed valuations.

This works even if top-line revenue is flat, provided utilization holds, and regulators don’t intervene.

1) Scenarios: Bull, Base, and The Cliff

Bull Case: The “GLP-1 Kicker”

The Narrative: The “Ozempic Boom” actually drives demand for skin tightening. Doctors realize they need InMode tools to fix the “deflated” look of weight-loss patients.

The Outcome: Consumables revenue re-accelerates. Margins stay high. Management retires 5% to 7% of the float annually. Double-digit earnings per share growth returns.

Base Case: The Grinding Cannibal

The Narrative: Hardware sales remain choppy. Consumables don’t skyrocket, but they don’t roll over. The business stabilizes as a cash cow.

The Outcome: Returns are driven almost entirely by the shrinking share count. It’s a grind, but a profitable one.

Bear Case: The Melting Ice Cube Accelerates

The Narrative: Technology moves on. Doctors switch to a competitor’s shiny new toy. Utilization drops.

The Outcome: Cash generation evaporates, buybacks stop, and the stock is a value trap. Permanent capital impairment.

2) Key Numbers (The Pulse Check)

Installed Base: ~29,000 systems. (The “Track”)

Consumables Signal: +26% YoY growth (in the most recent cited quarter).

**This is the most important number. If hardware is down but consumables are up, the thesis is alive.Gross Margin: ~78%. (High margins = more fuel for buybacks).

Share Count Reduction: Down to ~64M from ~86M in 2023 (~25%)

Buybacks Deployed: ~$285M in 2024 alone.

3) Kill Switches

If any of these are triggered, the thesis is broken.

Utilization Inversion:

Trigger: Consumables growth drops below installed-base growth for two consecutive quarters.

Why it matters: Utilization per machine is falling. The toll road is closed.

The “Diworsification” Pivot:

Trigger: Any acquisition >$100M.

Why it matters: Management has run out of ideas. The “Cannibal” phase is over; the “Empire Building” phase has begun.

The Regulatory Gavel:

Trigger: Escalation beyond the FDA Warning Letter.

Why it matters: The FDA issued a Safety Communication on RF in late 2025. Further escalation or a Class I recall could be a lethal trigger.

4) Valuation: The “Haircut” Model

In a distressed scenario, we don’t use optimized numbers. We use “apocalypse” numbers.

Market Cap: ~$896M

Net Cash: ~$530M -> Haircut by 20% for “Geopolitical/Trapped” risk -> ~$425M adj. cash.

Implied Enterprise Value: ~$471M

Operating Income: ~$96M

The Multiple: ~4.9x Operating Income.

The Takeaway: Even if we assume that 20% of their bank account disappears due to war or taxes, we’re paying less than 5x earnings for a business with 78% gross margins.

Conclusion

InMode is no longer a “growth” stock. It is a time-arbitrage play. It is a bet that the installed base is stickier than the market thinks, and that management will continue to eat its own stock.

If Burlington Northern taught us anything, it’s that you don’t need to get bigger to get rich. You just need to get smarter about what you own. As long as InMode keeps shrinking the share count faster than the lasers cool down, the math works.