On Multibaggers and Endurance

What an empirical analysis of 464 outliers reveals about the true nature of compounding capital.

In 2016, a marine biologist pulled a Greenland shark from the freezing waters of the North Atlantic. Radiocarbon dating of its eye tissue revealed that the animal was nearly 400 years old.

It was swimming in the ocean before the United States existed.

It survived centuries of shifting ice ages and industrial whaling not by being the fastest swimmer or the most ferocious apex predator. It survived by adapting to brutal conditions and conserving energy to outlast its competitors.

It won the evolutionary game through unmatched endurance.

Most investors spend their lives hunting for the fastest swimmers. They chase short-term earnings and obsess over rapidly scaling tech startups. But consensus analysts fail to realize that extreme wealth creation requires an entirely different makeup.

The stock market is often a brutal environment for capital.

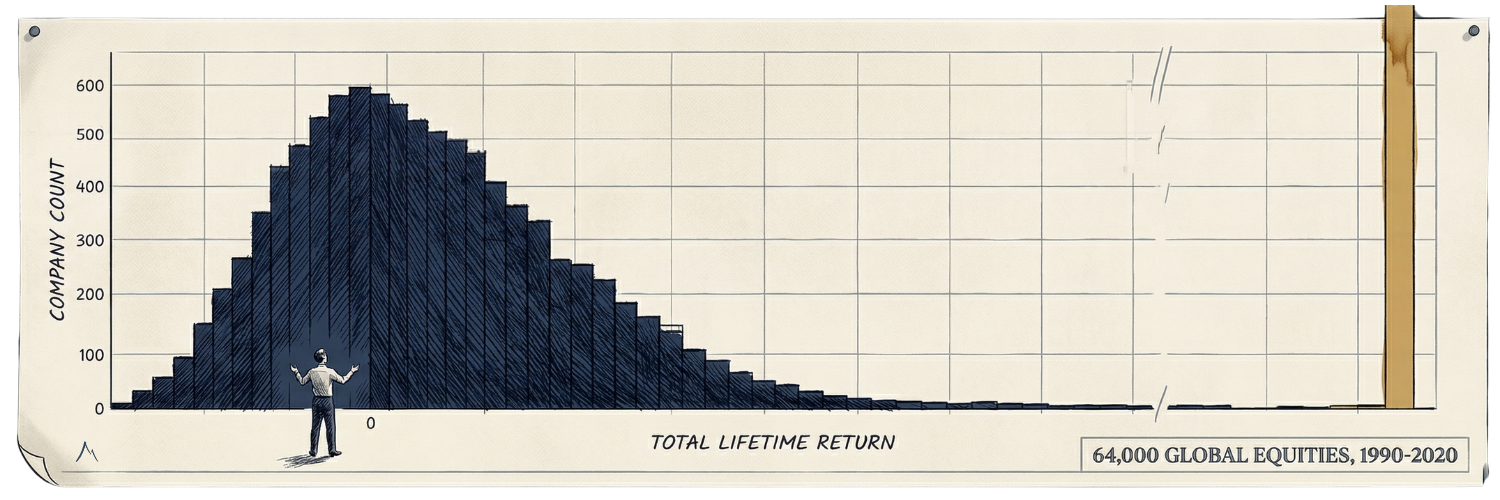

Research by Arizona State University professor Hendrik Bessembinder, covering 64,000 global equities from 1990 to 2020, uncovered a stark reality. For most individual common stocks, the most frequent outcome over a lifetime is a 100% loss. Capital is not merely underperforming. It is vaporized.

Furthermore, 55.2% of U.S. stocks underperform one-month U.S. Treasury bills. The historical return of the market is largely a statistical illusion, one that exists only because the losses of the majority are overwhelmed by the staggering returns of a microscopic fraction of outliers.

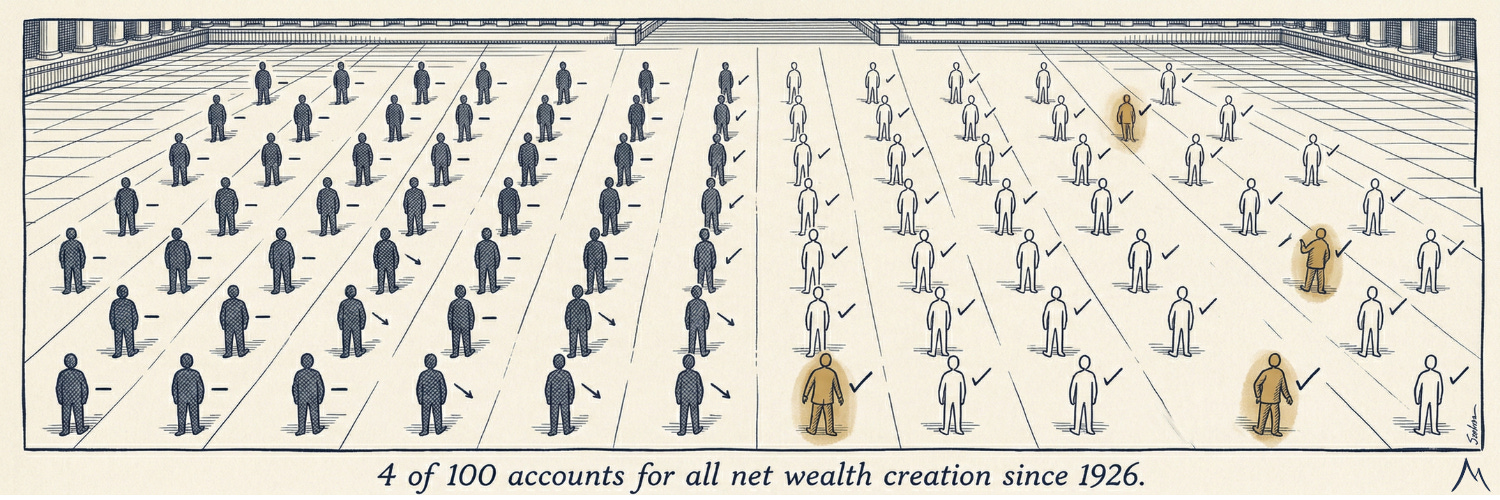

Bessembinder found that just 4% of listed U.S. companies account for all net wealth creation since 1926. The other 96% collectively matched the return of cash sitting in a bank account.

Getting rich and staying rich require different skills. But generating multigenerational wealth requires finding that 4% and refusing to let go.

The Anatomy of an Outlier

Legendary investor Peter Lynch famously coined the term “multibaggers” to describe these rare anomalies. Today, we have a blueprint of their anatomy before they scale into market giants.

Sell-side analysts claim the secret is rapid top-line growth, building elaborate spreadsheets to project earnings for disruptive software companies. But they screen for the wrong traits entirely.

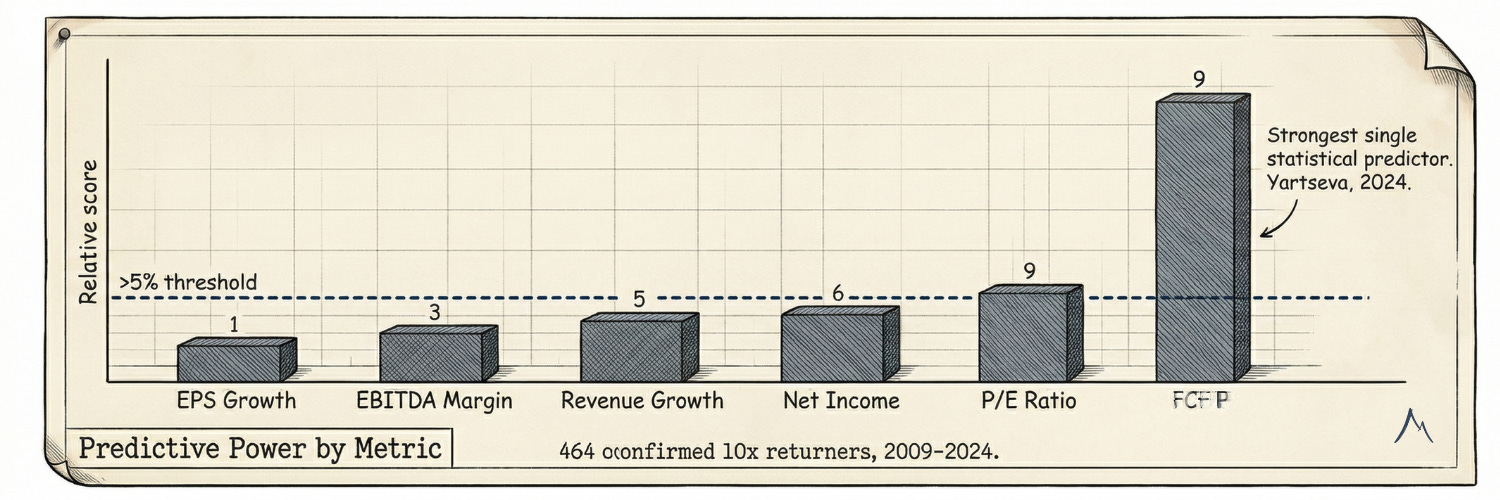

An empirical study by Anna Yartseva, which analyzed 464 “10-bagger” companies between 2009 and 2024, systematically dismantles the conventional playbook.

Her research shows that short-term earnings growth has no predictive power, and sector bias is a myth. The winners span broadly across consumer goods, industrials, healthcare, and utilities. Screening exclusively for undiscovered tech stocks filters out a massive portion of actual compounders.

Instead, the single strongest statistical predictor of an extreme outlier is astonishingly unglamorous.

Starting cheap relative to actual cash generation matters more than almost any other quantitative variable.

Buying a business at a steep discount to its free cash flow yield dwarfs almost every other metric. High book-to-market ratios combined with positive operating profitability form the true compounding engine of these firms. They generate massive owner earnings and rely on internal cash generation, rather than venture capital or Wall Street lifelines, to fund their operations. Downside-aware underwriting provides the margin of safety needed for multiple expansion and long-term survival.

Outsized returns are also heavily constrained by the limits of size. You cannot multiply a $100 billion company by 100 without absorbing an impossibly large share of the global ecosystem.

The median starting market capitalization for this dataset of 464 “10-baggers” was $348 million.

Expanding the research horizon to evaluate 100-baggers confirms this exact constraint.

The ideal entry window is a market capitalization between $200 million and $2 billion.

Overlooked by institutions due to a lack of immediate investment banking fees, these businesses operate in the shadows. Unearthing them requires a framework rooted in extreme skepticism, one that demands a falsifiable thesis and explicit assumptions before a position can be established.

The Ruthless Capital Allocator

Cheap cash flows and small market capitalizations only form the anatomy of the investment. Leadership determines its survival.

The highest-returning multidecade compounders are rarely led by visionary product marketers. They are directed by ruthless capital allocators. As author William Thorndike documented in his research on corporate “outsiders,” executives who generate multigenerational wealth view their primary job not as operating a business but as allocating the cash the business generates.

They prioritize per-share value creation over aggregate corporate size. When their stock is mispriced, they cannibalize their own share count. When their industry panics, they execute disciplined countercyclical acquisitions while ignoring institutional demands for predictable quarterly guidance.

Historical outsiders like John Malone and Henry Singleton compounded capital at rates above 20% annually for over two decades. They understood that shrinking the share count while growing cash flow creates a dominant, twin-engine compounding organism.

These outliers rarely look the same on the surface:

The Toll-Takers: Companies like Constellation Software build essential infrastructure with recurring revenues and switching costs so high that displacement is effectively impossible.

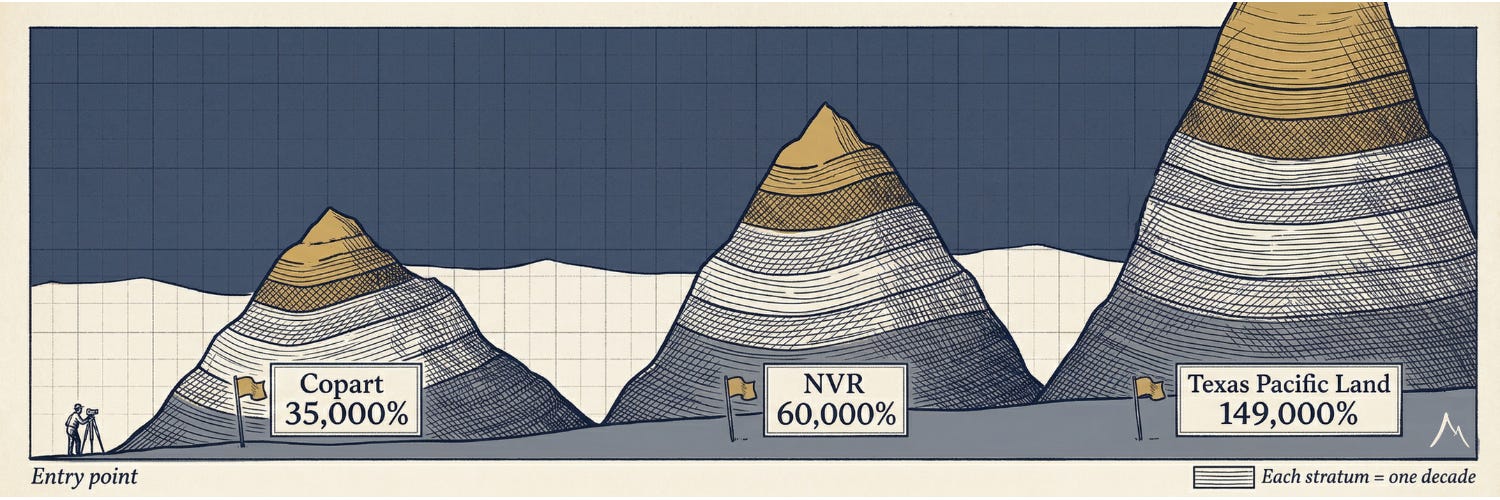

The Legacy Asset Compounders: Texas Pacific Land transformed from worthless desert into a royalty machine delivering a 149,000% return.

The Mundane Survivors: Perhaps the most fascinating examples operate in highly unglamorous sectors.

Copart revolutionized the auto salvage industry by moving junkyard auctions online, building a global duopoly that generated a 35,000% return.

NVR abandoned the capital-intensive land development model typical of homebuilders, utilizing land options to return nearly 60,000% over three decades.

HEICO quietly dominated the aerospace aftermarket by reverse-engineering replacement parts, compounding capital at 22% annually since 1990.

The market is constantly distracted by the flash of new trends. Generational wealth is built by holding the resilient anomalies.

The Psychology of Endurance

This framework sounds highly rational on paper. In practice, it is psychological torture.

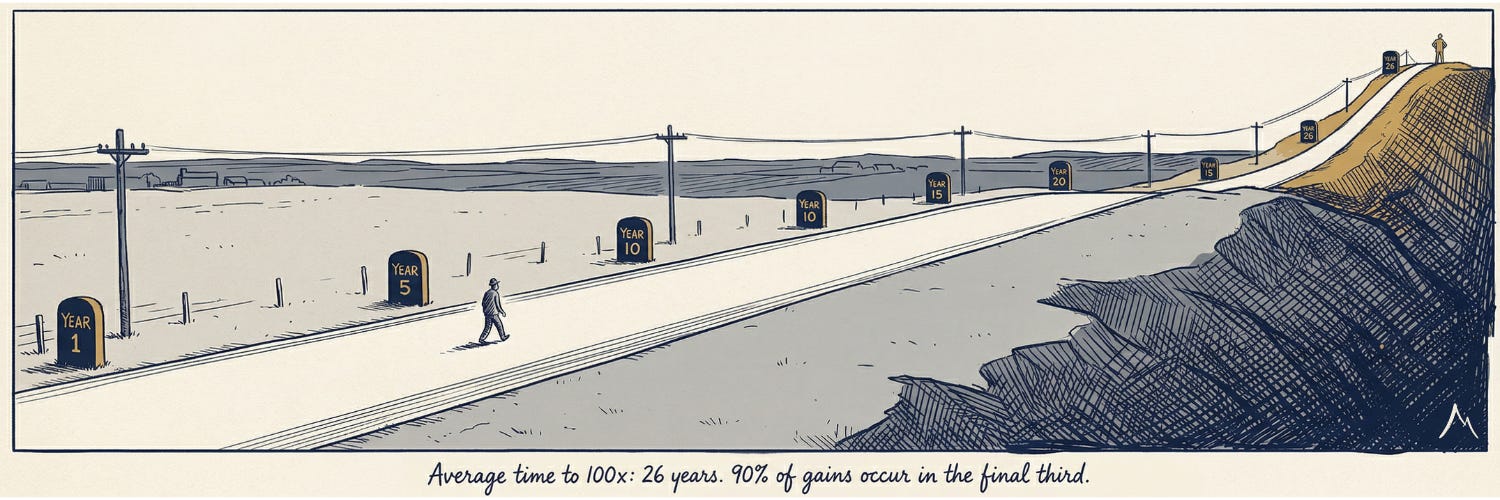

Achieving outlier status is fundamentally a test of duration. There is no shortcut that bypasses the mathematics of time. Author Chris Mayer studied every 100x-returning stock from 1962 to 2014 and found that the average time required to hit that milestone is 26 years. Even the absolute fastest-growing companies in history required nearly two decades of sustained 26% annualized returns to cross the finish line.

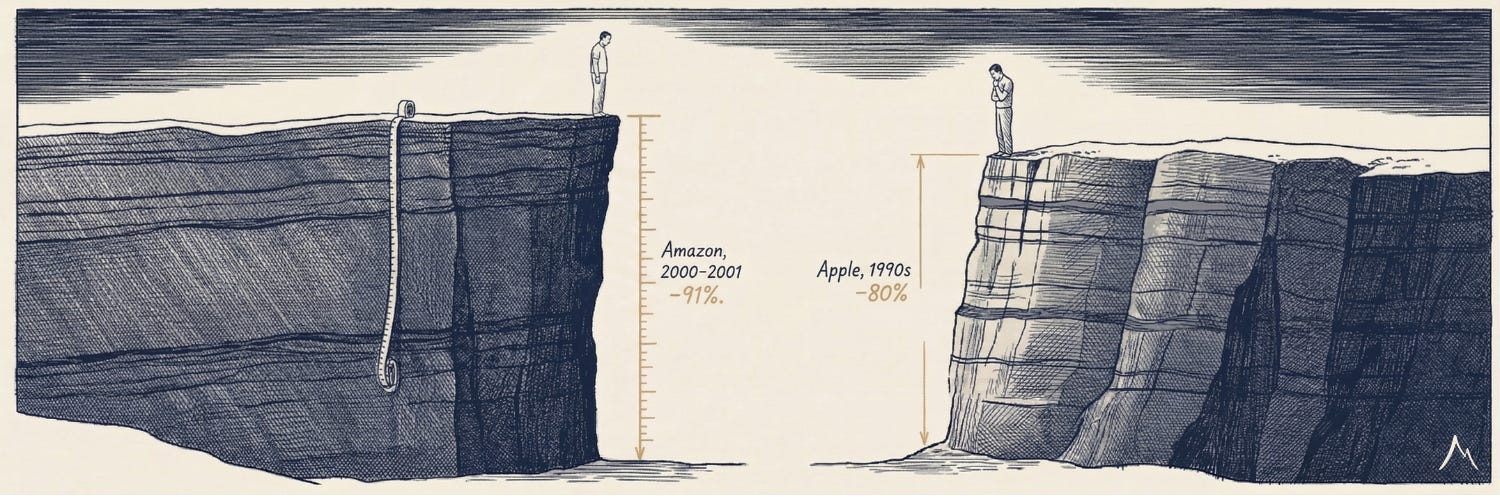

The journey is never a straight line. Apple stock fell 80% in the 1990s and suffered three separate 70% drawdowns on its way to becoming a dominant ecosystem. Amazon lost 91% of its value between February 2000 and September 2001.

Imagine watching nine-tenths of your wealth vaporize and deciding to do absolutely nothing. It goes against every natural instinct we possess.

Our biological wiring is fundamentally hostile to long-term compounding. Morgan Housel perfectly captured this behavioral hurdle when he noted that an investor’s personal experience accounts for a microscopic fraction of global financial history, yet it shapes their entire worldview. Because of this localized bias, we are wired to panic when we see red on a screen.

The true barrier to capturing an exponential return is rarely analytical. It is behavioral.

Because the math of compounding is severely back-loaded, the vast majority of absolute dollar gains occur in the final years of the holding period. Premature selling is the ultimate destroyer of extreme wealth.

Surviving the Deep

Finding an underfollowed company with true moat durability and a founder buying back stock is only the beginning. The roadmap to generational wealth requires three distinct disciplines:

Find the Outlier: Identify the rare 4% with high free cash flow yields and ruthless capital allocators.

Demand a Margin of Safety: Buy at a steep discount to the cash the business generates.

Do Absolutely Nothing for 20 Years: Hold through global recessions, bear markets, and geopolitical crises.

The next generational compounder is hiding in plain sight today. It is a small company in a stagnant industry that generates massive free cash flow, is led by a disciplined capital allocator, and is ignored by consensus.

Finding an outlier requires outsmarting the crowd. Holding one requires surviving your own psychology.

The fastest swimmers eventually exhaust themselves.

The survivors compound in the dark.