The Anti-Supermarket: Compounding Capital by Selling Less

Sprouts abandoned the grocery wars to build a high-margin compounding machine. Here’s why the market just mispriced it.

In a basement passage beneath Tokyo's Ginza district, there is a restaurant with ten seats, no sign on the door, and a waitlist measured in years. The chef, now in his late eighties, has served the same menu in the same room for five decades. There is no à la carte. No substitutions. The meal lasts under thirty minutes and costs $300. The Michelin Guide awarded it three stars, the highest achievable rating. He is, by any serious measure, the greatest sushi chef alive.

Jiro Ono has been offered larger spaces, nicer locations, partner chefs, and expansion capital. He has refused everything. The offer that keeps coming is the same one every industry makes to anyone doing something well. Make it bigger, and you can serve more people. His answer, for fifty years, has been the same. If you serve more people, you stop serving them perfectly. And perfect is the only thing he knows how to sell.

The culinary world has never fully settled whether Jiro’s restraint is philosophy or stubbornness. The financial world, looking at the same problem in different industries, tends to assume that refusing to scale is simply a failure waiting to happen. Most of the time, this assumption is correct. Rarely, it is the most expensive mistake an analyst can make.

In 2019, a former Walmart grocery executive named Jack Sinclair arrived at a struggling specialty supermarket chain with 340 stores, mediocre margins, and an identity crisis. He immediately began removing things.

Sprouts Farmers Market (Ticker: SFM) began with a fruit stand. Henry Boney opened a small produce stall in San Diego in 1943, selling fruit to people who wanted produce first and everything else as an afterthought. The stand worked because it understood something most retailers spend decades trying to unlearn. The customer who knows exactly what they want is worth more than the customer who can be talked into almost anything.

The Boney family formalized this idea in 2002, building specialty grocery stores laid out like indoor farmers markets, with produce at the center and vitamins, bulk bins, and specialized dietary items radiating outward around the perimeter. It was a good concept in a bad competitive position. For most of its first decade, Sprouts tried to be two things at once: a curated health destination and a value-oriented deal machine. Every week, 21 million paper circulars landed in mailboxes, advertising loss leaders, competing on price with Kroger for the coupon-driven shopper who would abandon Sprouts the moment a cheaper option appeared. The mediocre margins reflected the identity.

Sinclair’s biography is the key to understanding what happened next. He had spent over a decade running Walmart’s U.S. grocery division, the most scale-obsessed food retail operation ever built. He arrived and concluded that Sprouts was already losing the game it was trying to play. Its target demographic of committed keto practitioners, gluten-intolerant shoppers, biohackers, and vegans with specific requirements could not be served well by a store that was also optimizing for bargain hunters.

Kroger’s best customer will drive to Costco if the price is right. Sprouts’ best customer cannot. When your diet is medically prescribed or metabolically committed, your grocery store is not a preference. It is infrastructure. Sinclair understood that a customer defined by price sensitivity is worth competing for only if you have Walmart’s scale. The customer defined by dietary necessity will walk past five other stores to reach the one that understands them. These are different businesses, and Sprouts was running the wrong one.

The customer who knows exactly what they want is worth more than the customer who can be talked into almost anything.

By 2020, he had executed one of the cleaner acts of strategic subtraction in recent retail history. He killed the print circulars. Ended the loss leaders. Stopped courting the deal-chasers who generated revenue but not profit. He reduced the blueprint for new stores from 30,000 to 23,000 square feet. He made explicit what Sprouts had always implicitly been: a store built for the roughly 15% of American grocery shoppers whose dietary commitments make them largely immune to competitive pricing. The result was a business that looks, from the outside, like a supermarket and earns, on the inside, like something else entirely.

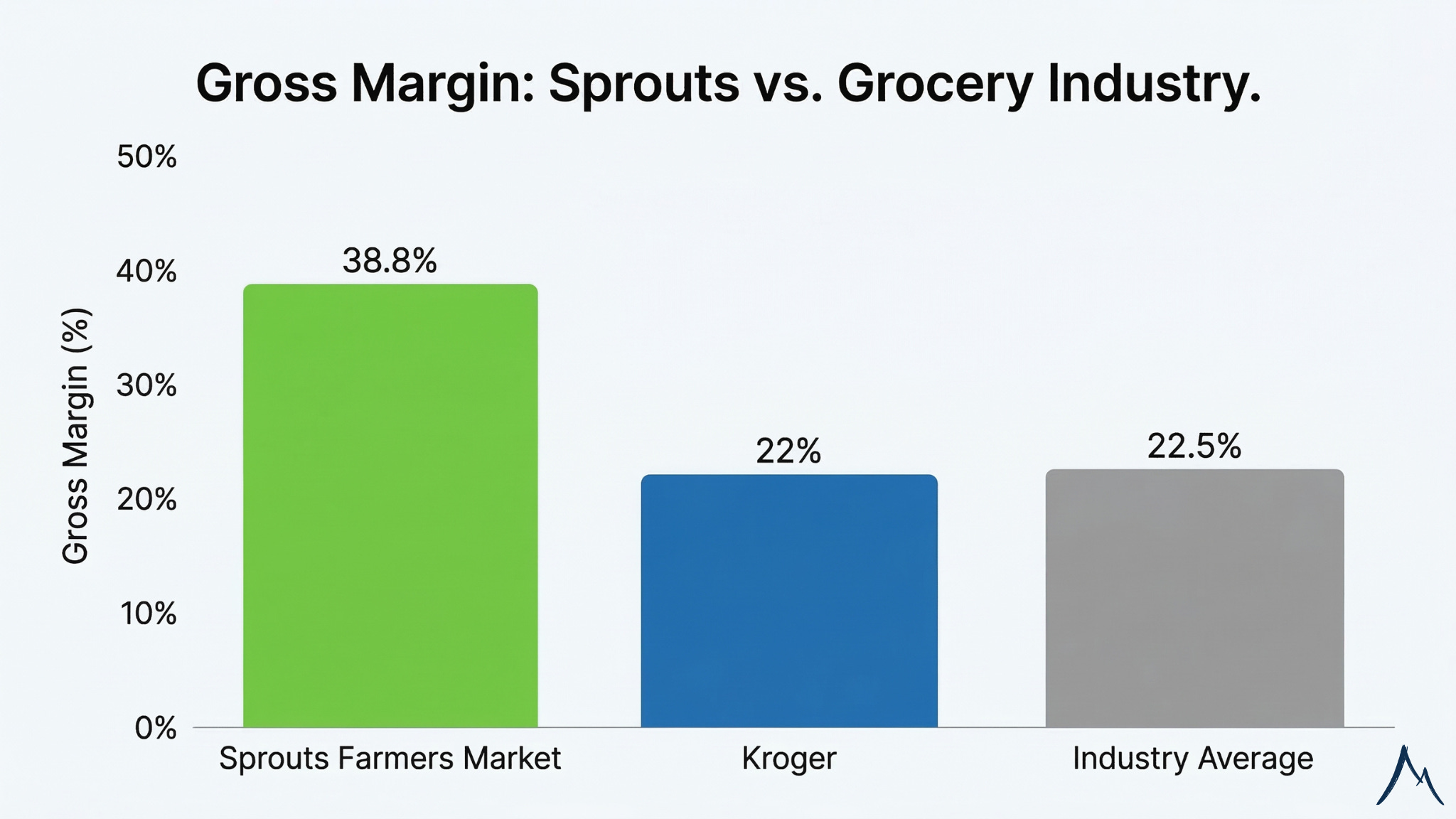

Here is what the grocery industry is supposed to look like. Kroger, the second-largest chain in America, runs gross margins around 22%. Net profits average roughly 1.7 cents on every dollar of revenue. This is not mismanagement. This is simply the physics of a commodity business selling the same box of Cheerios as every competitor within five miles.

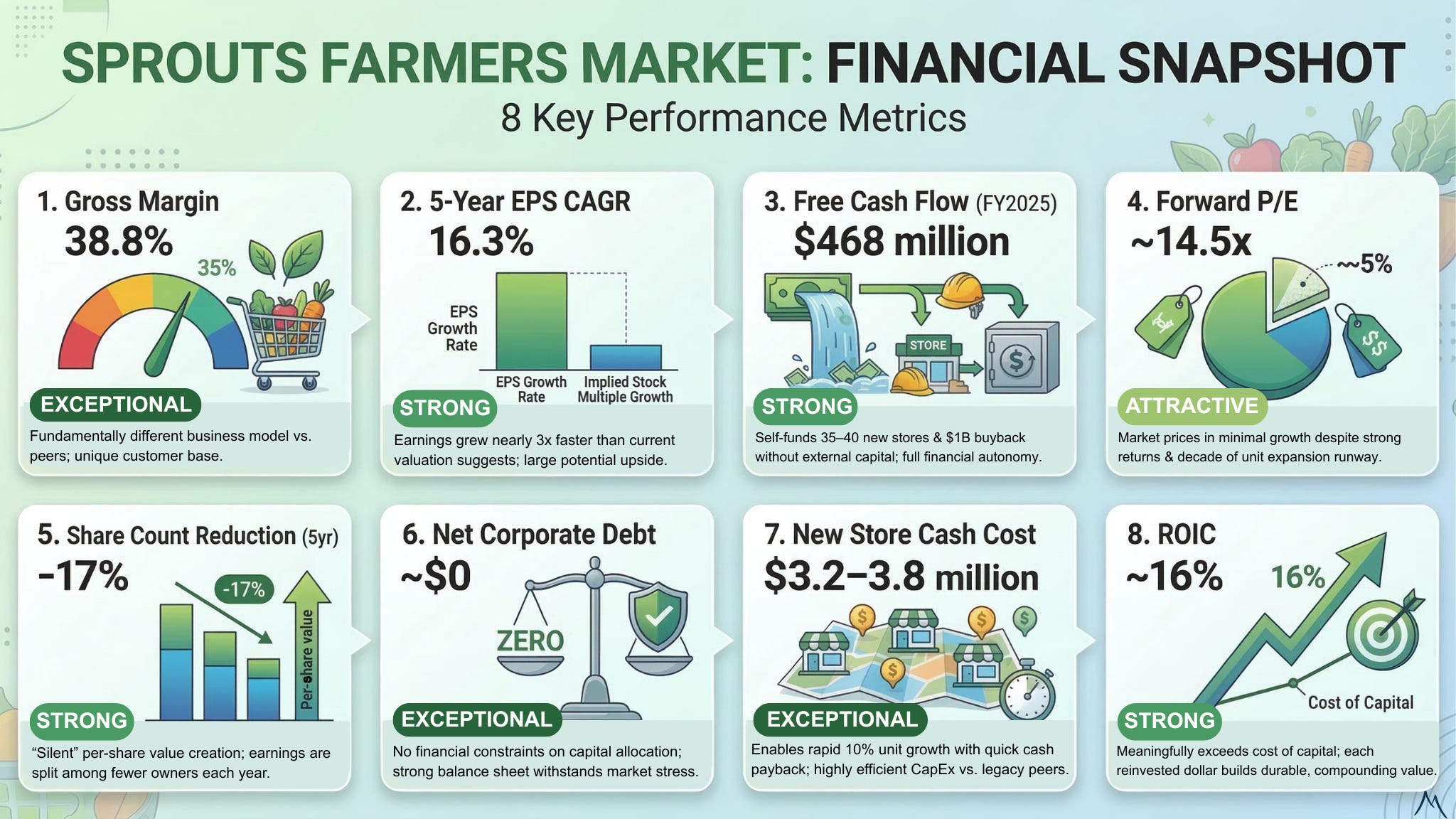

In a grocery business selling perishable food, Sprouts’ gross margin in 2025 was 38.8%. The first time you encounter that number, it reads like a typo.

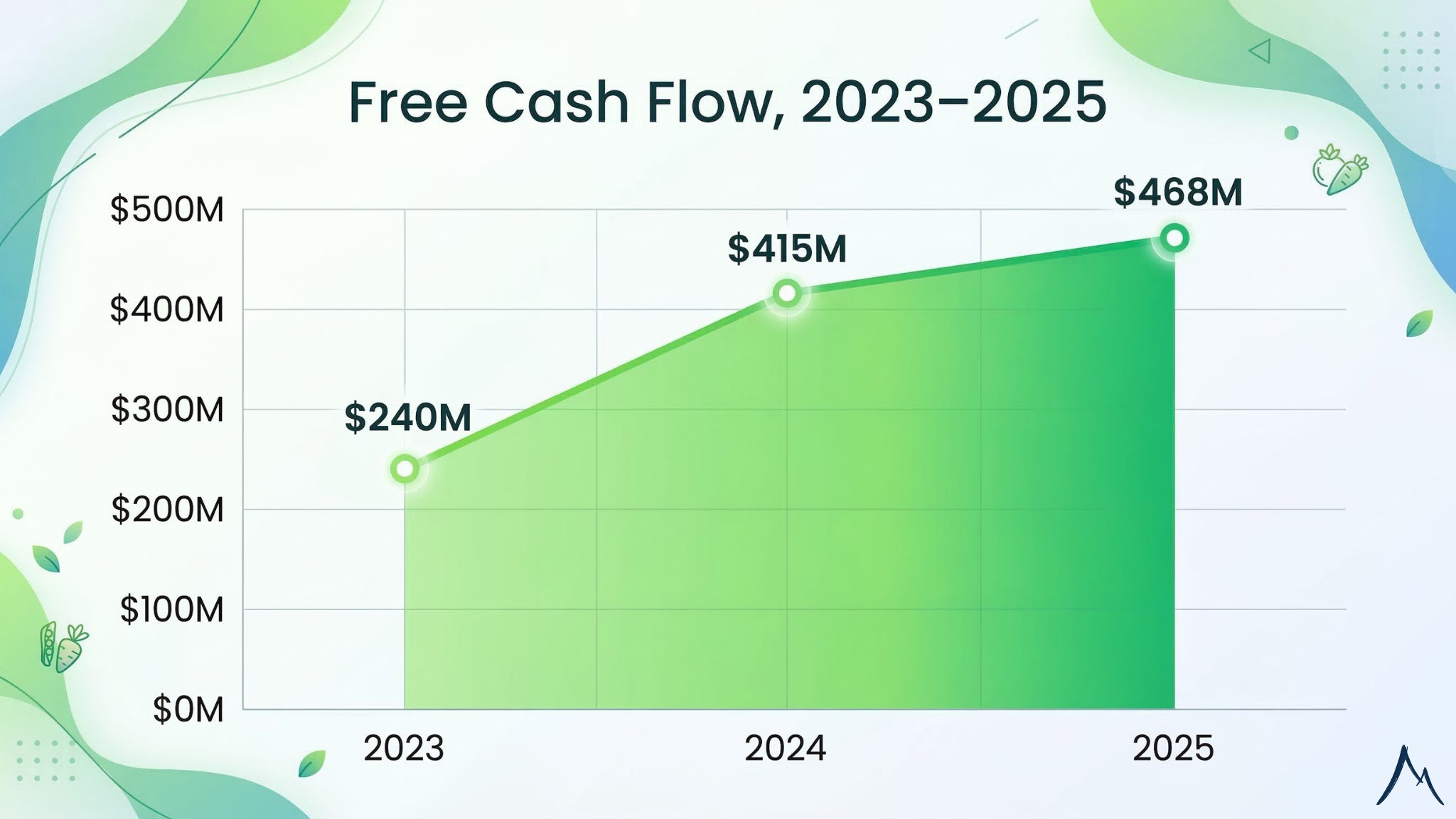

The transformation did not arrive suddenly. In 2022, gross margins were 36.7%. By 2024, 38.1%. Quietly, each year, the business got more profitable per dollar of revenue, not because prices rose, but because the promotional drain was gone and the customer mix had shifted entirely toward people who come for curation, not deals. Free cash flow traced the same arc: $240 million in 2023, $415 million in 2024, $468 million in 2025. Nearly doubling in two years while opening dozens of new stores annually.

A new Sprouts costs between $3.2 million and $3.8 million in cash to open. A conventional grocery buildout runs multiples of that figure. That gap is not clever negotiating. It is a consequence of what the store is not. No pharmacy. No apparel section. No bank branch. No tire center. And roughly 80% of Sprouts’ locations sit within 250 miles of a distribution center, a geographic discipline that keeps produce spoilage near zero and the entire margin structure intact. The machine is not just efficient. It is designed to stay efficient as it grows.

One number reframes the entire business.

Sprouts has reduced its share count by 17% over five years, from roughly 118 million shares to under 98 million, funded entirely from operating cash, with zero net debt on the balance sheet.

Each remaining share now owns a larger fraction of a more profitable business than it did five years ago. That is compounding working in two directions simultaneously, without anyone writing a check.

The market looks at Sprouts, places it next to Kroger and Albertsons in a spreadsheet, and assigns it a grocery multiple. This is not irrational. It is mechanical. Sector classification is how analysts manage cognitive load across hundreds of names, and Sprouts’ SIC code says “supermarket,” so supermarket multiples apply. The problem is that Sprouts is not competing in the same business as Kroger. It is competing in a different business that happens to use similar-looking buildings. Valuing Sprouts on a grocery multiple is roughly as useful as pricing Ferrari on the same earnings multiple as General Motors because both companies manufacture cars.

We judge things by their containers. The label on the jar tells us what’s inside.

In early 2026, Sprouts guided for approximately flat comparable-store sales, a predictable consequence of lapping a prior-year base inflated by exceptional health-food demand. Algorithmic systems read “negative comps” and sold aggressively. The stock fell more than half from its 2025 highs. What the systems did not model was the difference between a business that is structurally slowing and a business being measured against a previous version of itself that had an unusual tailwind. The margin structure did not change. New-store economics did not change. The share count kept falling. The board authorized a new $1 billion share repurchase program. Several directors began buying personally in the open market.

When a board member starts buying company stock with their own money, they are not making an argument. They are making a bet.

Markets are efficient at pricing information. They are less efficient at pricing the difference between a temporary hangover and a structural impairment, particularly when both, at a glance, produce the same negative comp number.

Jiro Ono once told a documentarian, in effect, that the secret to his restaurant was not knowing what to cook. It was knowing what to refuse.

Sprouts refused Coca-Cola. Refused Tide detergent. Refused 21 million paper circulars and the bargain-hunters who followed them. Refused 7,000 square feet of floor space that would have made the stores feel normal. The result is a business with grocery margins that rival a consumer software company, a balance sheet with no traditional debt, and many years of runway to keep building smaller stores in parking lots where no one else sees the opportunity.

The most restricted restaurant in Tokyo has been full every night for fifty years. The question Sprouts poses is whether the same logic of refusal as strategy and limitation as leverage works in suburban America.

The evidence so far says yes. The current valuation suggests the market hasn’t decided yet. The most durable compounders rarely look like compounders when they’re cheap.

EXECUTIVE VERDICT: Strong Candidate

Sprouts is a high-quality specialty retailer operating with the unit economics of a niche consumer brand. By completely abandoning commodity pricing and leveraging dietary convictions as structural switching costs, Sprouts commands gross margins nearly 75% above the grocery average. Yet, the market systematically mislabels it as a commodity grocer.

The business has demonstrated durable gross margin expansion across three consecutive years. Its compounding engine runs on these expanding margins, internally funded new-store growth, and continuous share buybacks that mechanically amplify per-share earnings regardless of same-store trends.

The market is currently mistaking a 2026 base-effect lapping issue for structural deterioration in demand. As a result, a 14.5x forward multiple prices in near-zero growth for a business compounding EPS at 16.3% annually. While physical retail carries inherent margin ceilings, and the health-conscious consumer is not entirely immune to cyclical macroeconomic pressures, the setup here is highly asymmetric. Backed by $468 million in annual free cash flow, zero traditional debt, and open-market insider purchasing, the current valuation offers a compelling entry point for any investor with a multi-year time horizon.

THE 8 NUMBERS THAT MATTER

#1. 38.8% (Gross margin): A level of structural profitability that traditional, legacy grocers simply cannot replicate.

#2. $3.2M to $3.8M (New store cash cost): Lean capital expenditure that enables rapid cash-on-cash paybacks and allows the company to confidently execute a 10% annual unit growth rate.

#3. $0 (Net corporate debt): A pristine balance sheet that poses no threat to the business model under stress and leaves management with zero financial constraints on capital allocation.

#4. $468 Million (FY25 free cash flow): Fully self-funds the rollout of 35 to 40 new stores per year while simultaneously executing a massive $1 billion share buyback program, without a single dollar of external capital.

#5. 16% (ROIC): Meaningfully above the company’s cost of capital, ensuring every reinvested dollar creates durable value.

#6. 17% (Share count reduction): The percentage of outstanding shares retired over the past five years. Each remaining share now owns a larger piece of a more profitable business.

#7. 16.3% (5-year EPS CAGR): The mechanical result of the company’s operating performance and aggressive, self-funded capital return program.

#8. 14.5x (Forward P/E multiple): A valuation that completely ignores a company deploying capital at high returns into a massive domestic white space, treating it instead as a stagnant grocery chain.

WHAT MUST REMAIN TRUE

The bullish case is entirely conditional. The following operational realities are the load-bearing walls of the investment thesis:

Strict Geographic Discipline: Accelerating expansion must not come at the expense of the 250-mile supply chain radius. The remarkably low-spoilage economics driving the fresh produce margin advantage rely completely on proximity to distribution centers.

Format Portability: As the company launches 35 to 40 locations annually across the Pacific Northwest, Midwest, and Northeast, the format must prove it can travel outside its historical strongholds in the Southwest and Southeast.

Rejecting Mainstream SKUs: Leadership must withstand any macroeconomic pressure to introduce conventional consumer staples. Adding high-volume commodity goods to artificially boost traffic would instantly dilute margins and destroy the brand identity. The day Sprouts stocks Coca-Cola is the day the investment thesis demands fundamental reassessment.

WHAT COULD BREAK THE THESIS

The following observable signals would indicate that the structural foundations are breaking down:

Gross margins drop below 37% for two consecutive quarters: This suggests a structural reversal driven by competitive pricing pressure, the reintroduction of promotional mechanics, or unpassable input cost inflation.

Comparable store sales remain negative through Q3 2026: If comps remain flat or negative as year-over-year comparisons ease, it indicates the recent acceleration was driven by one-time demand rather than structural share gains.

New store productivity misses underwriting targets: If first-year sales volumes in new geographic regions track materially below historical baselines, the geographic portability of the format is unproven.

Amazon closes the affordable specialty gap: If Amazon deploys systematic, Prime-subsidized pricing in the $10 to $25 fresh basket range and sustains it long enough to shift consumer habits, the Sprouts positioning moat narrows.

THE MONITORING DASHBOARD

The thesis relies on relentless execution. Monitor these specific metrics quarter by quarter to validate the model:

Comparable store sales: A return to positive same-store sales by the third quarter of 2026.

The gross margin floor: Maintenance of the 38% baseline.

Geographic portability: First-year sales volumes for new store openings outside the Sunbelt meet historic underwriting targets.

Private label penetration: Directional expansion beyond the current 21% to 25% baseline, indicating a healthy product innovation engine.

Capital return execution: Aggressive deployment of the newly authorized $1 billion share repurchase program at current valuation levels.

Bedrock Capital Research is an independent research and education publication, not a registered investment adviser or financial planning service. Nothing published here constitutes personalized investment advice, a solicitation to buy or sell any security, or a substitute for guidance from a qualified professional who understands your specific circumstances. Click HERE for full disclosures.