The Cult of UGG-ly Utility

A $2.5 billion brand. Zero respect. One opportunity.

In 1972, a surfer named Brian Smith brought a pair of Australian sheepskin boots to California. They were objectively hideous. They looked like baked potatoes for the feet. But they possessed one trait that would eventually build a global empire: they were unapologetically functional. Surfers wore them because they warmed frozen feet faster than anything else on earth.

Wall Street and the fashion industry saw a fad. They assumed a product this aesthetically challenged had an expiration date tied to a passing trend. They underestimated the narcotic power of physical comfort.

In 2009, two French trail runners designed a shoe with a comically oversized, marshmallow-like midsole. It violated every minimalist design rule in athletic footwear. It looked ridiculous. But for ultra-marathoners and nurses working 12-hour shifts, the extreme cushioning solved a real and painful problem.

Wall Street looked at HOKA and saw another niche fad. They were wrong again.

Both brands belong to Deckers Outdoor (DECK). And today, the market is looking at the same company and making the exact same mistake.

Wall Street chronically misprices ugly utility. Financial models are excellent at measuring top-line growth, but they are terrible at measuring the cult-like loyalty of a consumer whose physical discomfort has been solved. When a brand prioritizes extreme functionality over aesthetics, it doesn’t just win customers. It wins evangelists.

More importantly, ugly utility creates superior unit economics. Because these products are purchased for function rather than fashion, they do not go out of style at the end of a season. That means Deckers rarely has to dump inventory on clearance racks. This behavioral dynamic is the invisible engine behind the company’s financial profile.

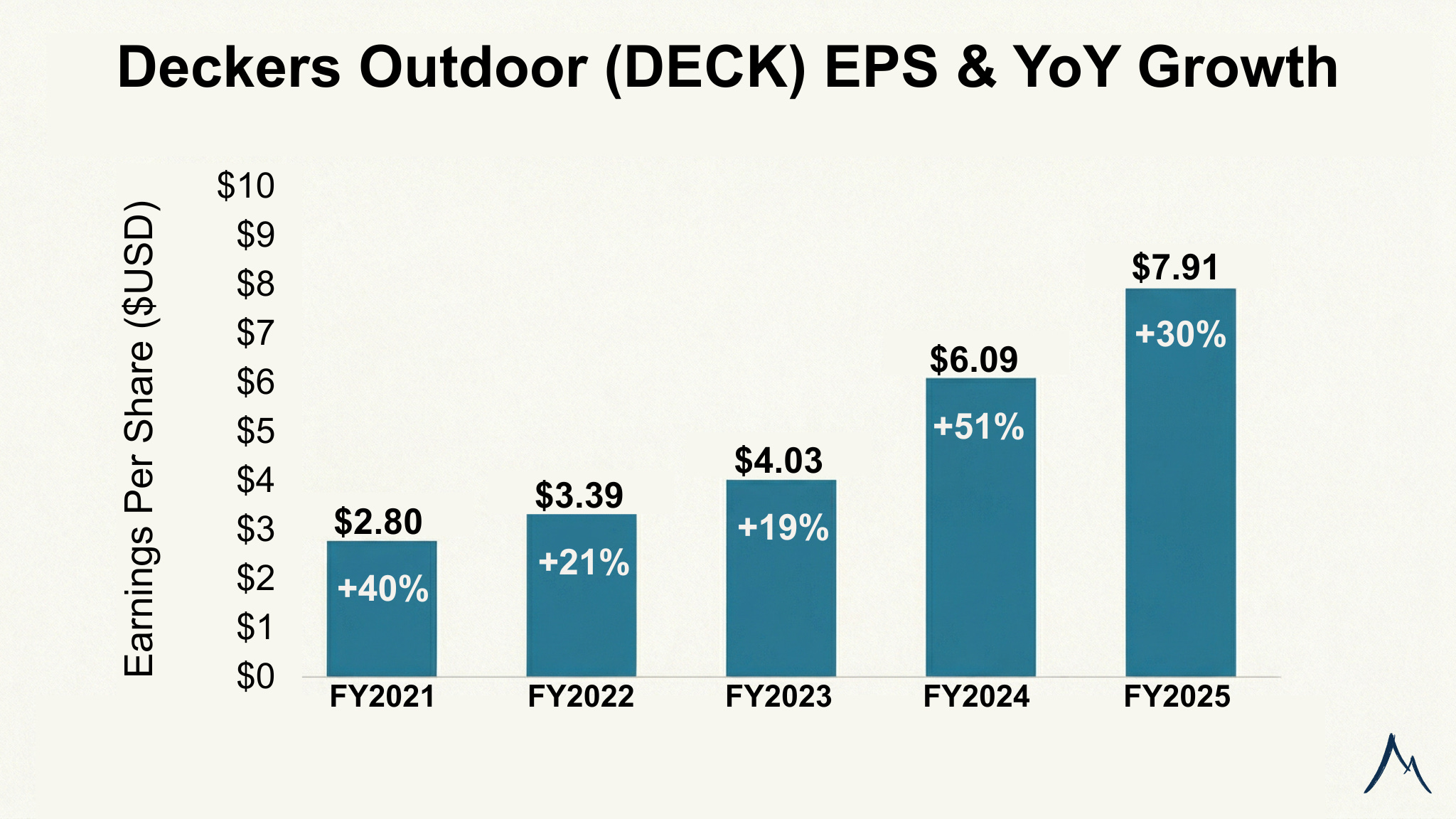

Today, the market has decided the Deckers growth story has permanently stalled. HOKA, which was growing at 35% in early fiscal 2025, decelerated to roughly 10% by the fourth quarter. Tariff fears dominated the headlines. Following a 50% drawdown, the market’s working assumption shifted from “global compounder” to “peaking fad.”

The cash flow statement suggests the market is hallucinating.

Last year, Deckers generated $958 million in free cash flow. It converts nearly 20 cents of every revenue dollar into pure cash. That is not an apparel metric. That is a software metric.

Yet Wall Street is pricing this business at 14x forward earnings. A 14x multiple belongs on a mature, capital-heavy business facing secular decline. It does not typically belong on a company that generates an 87.7% return on invested capital, sits on $1.89 billion in cash, and carries zero long-term debt.

The market is betting the Deckers story has reached its final chapter. History suggests Wall Street simply doesn’t understand the genre—and is mispricing the sequel.

THE COMPOUNDER VERDICT

Executive Classification: Strong candidate; elite quality at a value multiple.

Deckers presents a rare dislocation between business quality and market multiple. The market has priced in permanent deceleration, discounting HOKA’s international runway entirely and ignoring a decade of demonstrated UGG resilience. It falls short of an “Elite” classification only because fashion risk, even in utility-first footwear, is never absolute zero. However, at this valuation, the risk-reward asymmetry is heavily skewed toward the patient owner.

THE 8 NUMBERS THAT MATTER

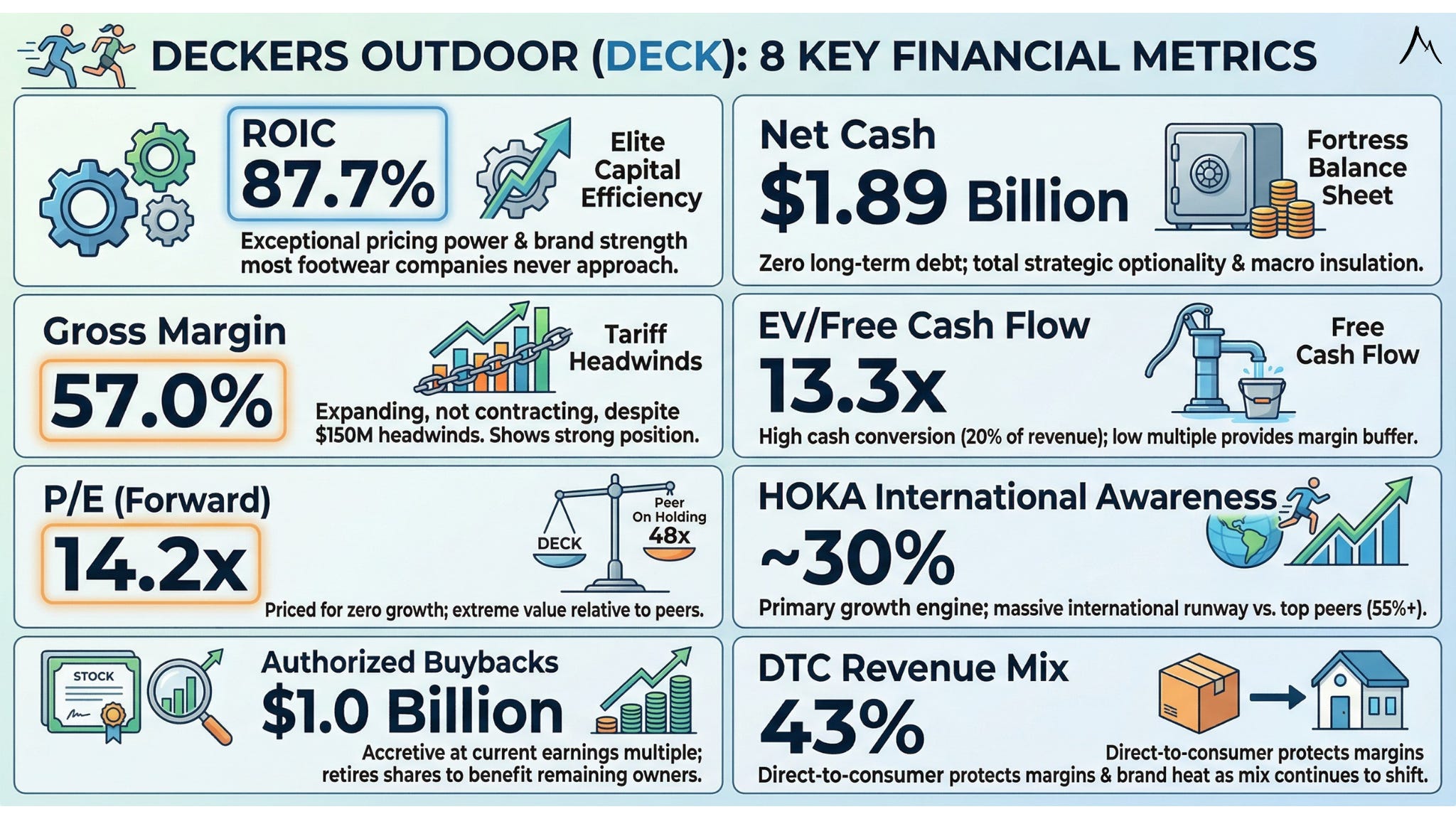

P/E (Forward): 14.2x. Deckers is priced for zero terminal growth. For context, peer On Holding trades at 48x.

EV/Free Cash Flow: 13.3x. A rare low-teens multiple for a business converting 20% of revenue to cash, providing a massive buffer against margin compression.

ROIC: 87.7%. Elite capital efficiency, signaling exceptional pricing power and brand strength that most footwear companies never approach.

Gross Margin: 57.0%. Expanding, not contracting, despite $150M in tariff headwinds. That is not a company in structural decline.

Net Cash: $1.89 billion. Zero long-term debt. The fortress balance sheet provides total strategic optionality and insulates the business from macro pressure.

Authorized Buybacks: $1.0 billion. At 14x earnings, every share management retires creates significant per-share accretion for remaining owners.

HOKA International Awareness: ~30%. The primary growth engine. Nike and Adidas pull 55%+ of revenue from outside the U.S. That gap is not a ceiling. It is a runway.

DTC Revenue Mix: 43%. Direct-to-consumer bypasses wholesale entirely, protecting both margins and brand heat as that mix continues to shift.

THE COMPOUNDER SCORECARD

Moat & Durability: 3.5/5. "Ugly utility" creates high switching costs in comfort categories. While physical products always face replication risks, UGG has proven multi-cycle durability, and HOKA is completing the transition from a running shoe to a global lifestyle staple.

Financial Fortress: 5/5. Flawless. Nearly $2 billion in cash, zero long-term debt, and 20% free cash flow margins.

Management Execution: 4.5/5. Masterful navigation of the 2025/2026 tariff shock. They absorbed costs, raised prices without killing demand, and protected gross margins.

Valuation Setup: 4.5/5. The current multiple provides a substantial margin of safety. The market is assigning a Skechers-level multiple to a business generating software-like capital returns.

WHAT MUST REMAIN TRUE

For this thesis to hold, Deckers must prove that it is not approaching a global growth ceiling.

International Expansion: HOKA's European and Asian growth must remain in the mid-to-high teens to offset stabilizing U.S. demand.

DTC Strength: Direct-to-consumer sales must stay above 40% of total revenue to protect the 57% gross margin profile.

Pristine Inventory: Inventory growth must trail revenue growth. If inventory growth outpaces revenue growth for two consecutive quarters, it signals the brand is cooling and management is stuffing the channel to mask the decline.

WHAT BREAKS THE THESIS

The Fashion Pivot: If management attempts to redesign UGG or HOKA to be sleek or trend-chasing, they will destroy the core utility value proposition and alienate the evangelists who built both brands.

Wholesale Dilution: If HOKA begins appearing in discount retailers to juice short-term revenue, the premium brand aura evaporates quickly and does not easily recover.

THE VALUATION FRAME

At an enterprise value of $12.75 billion (roughly 10.2x EBITDA and 14x forward earnings), the market is explicitly pricing Deckers as a 5% terminal growth business. It assumes the $2.5 billion HOKA brand has tapped out its global total addressable market in less than 15 years, and that current margins represent a cyclical peak.

If HOKA’s growth permanently settles at high-single digits and UGG reverts to a seasonal novelty, 14x earnings is a fair price.

But if HOKA’s 30% international brand awareness climbs toward the 60% standard set by legacy incumbents, and management uses its $1 billion buyback authorization to aggressively retire shares at this compressed multiple, the current price is a severe miscalculation.

The skeptics have already written the final chapter of this company. They might be right. But for a business with zero debt, 87% ROIC, and a multi-decade history of turning ugly utility into billion-dollar empires, that is a very expensive assumption to bake into a price.

Bedrock Capital Research is an independent research and education publication, not a registered investment adviser or financial planning service. Nothing published here constitutes personalized investment advice, a solicitation to buy or sell any security, or a substitute for guidance from a qualified professional who understands your specific circumstances. Click HERE for full disclosures.